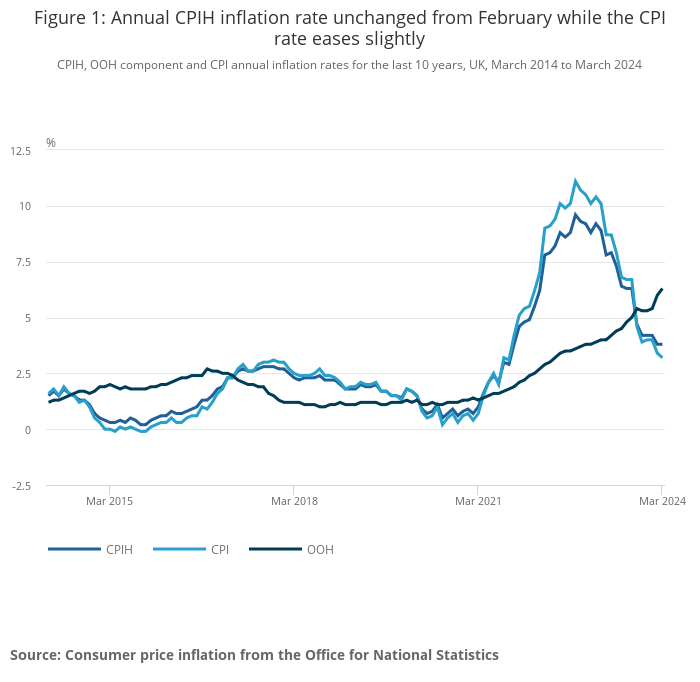

Inflation has been very high in the UK recently, as the graph shows. And whilst inflation is now falling, overall Owner-Occupier Household (OOH) costs are still rising, adding another suppressant to house prices (or at least household income).

But there are some upsides – because inflation, often seen as a financial villain, can actually play the role of a silent hero in the world of property investing and debt management. While it erodes the purchasing power of money over time, it also erodes debt.

For property investors, inflation acts as a powerful ally, driving up the value of tangible assets. As the general price level rises, so do property values, making property an effective hedge against inflation.

Similarly, inflation can benefit debtors by reducing the real burden of debt. As prices rise, the value of money declines, effectively reducing the relative size of outstanding debts. Just think of a pint of milk – it is worth (probably) the same to you today as it was 20 years ago (so many cups of tea etc), but it cost about half as much 20 years ago. It’s not the value of milk that’s gone up – it’s the value of the money that has decreased. This is why having lots of money sat in bank accounts is generally a very bad idea – especially now. It loses value over time. For borrowers with fixed-rate mortgages, inflation erodes the real value of their debt, making it easier to repay over time. This phenomenon, known as “inflation erosion,” allows debtors to repay loans with less valuable currency, effectively reducing their debt burden in real terms.

By understanding and leveraging the power of inflation, investors and debtors can navigate economic uncertainties and build wealth over the long term.

Discover more from Married2Property

Subscribe to get the latest posts sent to your email.